Why Can't China Bail Out It's Banks?

The Saga of Shengjing and Evergrande

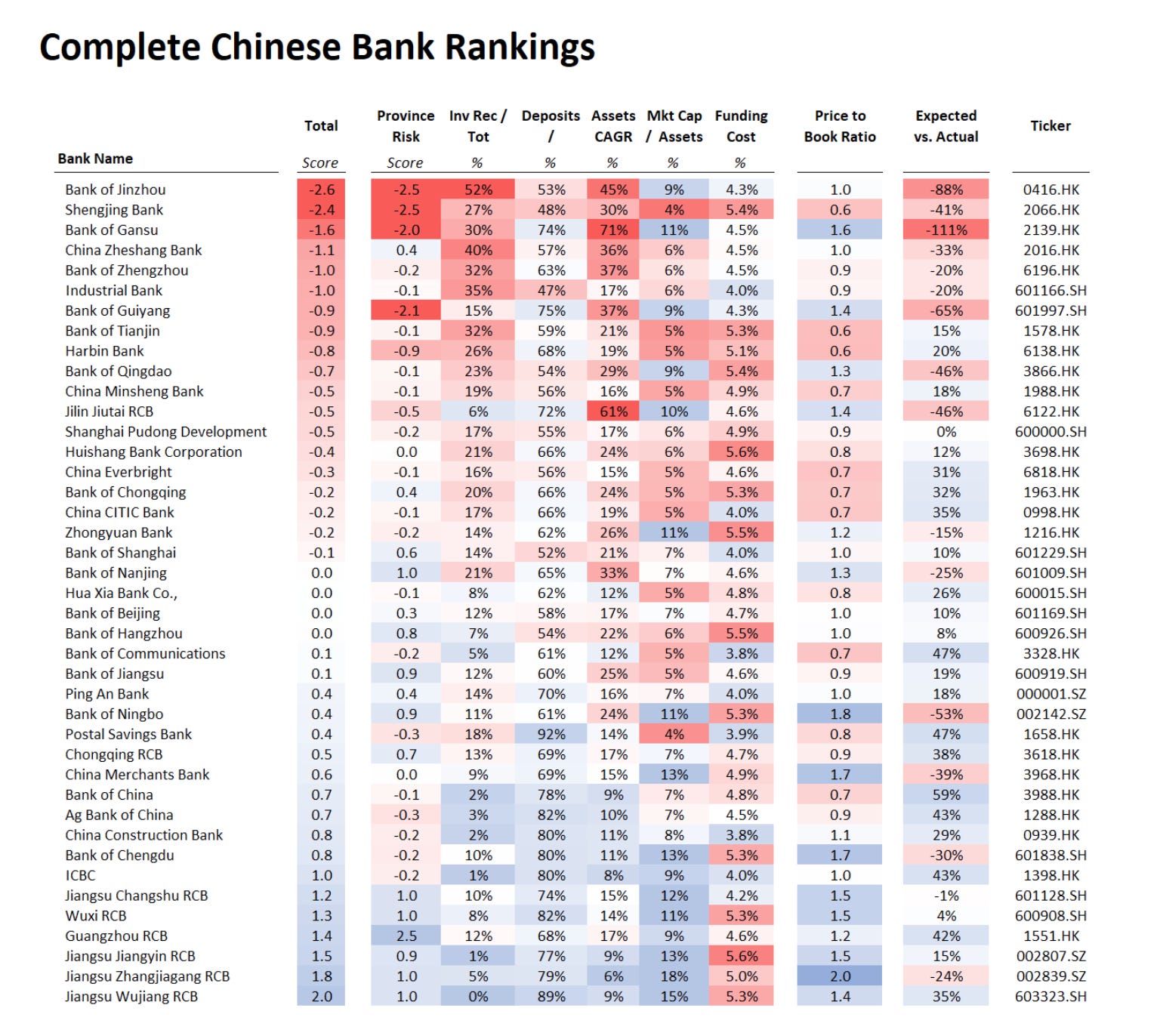

You probably haven’t heard of Shengjing Bank (2066.hk)…

Back in 2018, a friend and I put together a report looking for “China’s Worst Banks”

Shengjing Bank, a small lender out of Liaoning, was at the top of our list.

Funny, only in China would a $150bn financial institution be considered ‘small’

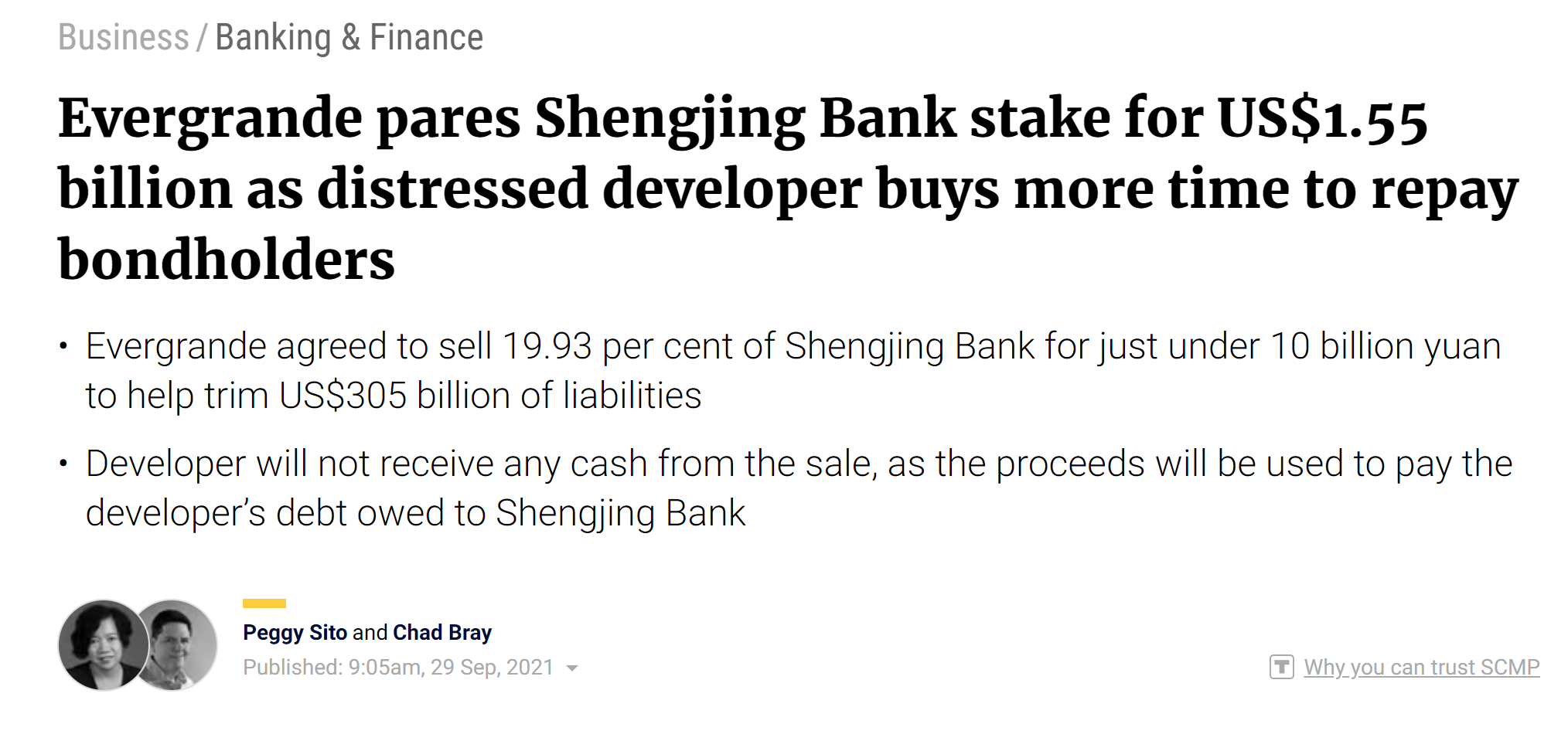

So imagine our surprise when a little over a year later, Shengjing was bailed out by Evergrande, of all people.

When was the last time a bank was bailed out by a property company?

When was the last time the rescuer paid 40% over market to do so?

This bailout, along with a suspension in the shares, managed to stabilize the situation for a couple of years.

Until two years later, when Evergrande was facing it’s own financial difficulties, and sold part of their stake for $1.5bn.

The lead buyer was Shenyang Shengjing Financial Holdings Investment Group.

Good luck trying to find their website, financials or any employees.

Auspicious timing, as less than three months later, Evergrande defaults on it's debt.

Nine months laser, a creditor committee forces Evergrande to liquidate it’s remaining stake for ~$1bn. To a similarly opaque consortium of public and private buyers.

Not three months later, Shengjing announces it is SUING Evergrande to collect on $4.5bn. Threatening to seize the ~30% stake in Xinjiang Guanghui Industry Investment Group ‘pledged’ as collateral.

Again, interesting timing given the history.

Ever heard of someone suing the firm that bailed them out?

How about for more money ($4.5bn) than the amount of their bailout (~$2.5bn)?

Me either. Weird stuff, all around.

~~~

Last week, Shengjing announced a sale of $24bn of assets (~15% of book) to a local “AMC” (read: bad bank).

Taking a 7.7bn of write-downs on 176bn of assets isn’t that bad. Just a 4% loss. Pretty good deal!

You might think investors would like that deal?

Wrong.

Since the announcement, Shengjing’s shares are down 30%. Putting it pretty much exactly back where it was before it’s bailout by Evergrande, 5 years ago!

This week, we got news of another run on another ‘small bank’ (read: $34bn balance sheet) called Bank of Cangzhou after a social media post questioning how much exposure they had to Evergrande.

Unsurprisingly, the post has been taken down.

Raising a series of questions:

Why go through 5yrs of drama just for a measly $3bn bailout of Shengjing?

What kind of regulator let’s a property company bail out of a bank?

How about one that owes them $4.5bn?

How long is the left tail of small banks with material exposure to Evergrande?

What does that list of bad banks look like when you expand it to other distressed property companies: Country Garden, Kaisa, Sunac, Shimao, Aoyuan, Ronshine, Zhenro

What is this taking so long? Does China not have the capital to deal with the problem.

Perhaps more importantly, do they even have the institutional capacity to process potentially tens and hundreds of failed banks? Restructurings are difficult, expensive and time intensive, as we’ve seen.

In short, maybe they won't because they CAN'T.

Disclaimers

The risk from property sector and those small banks in China is closely related to local government debt, Trivium China recently published a post on how to defuse this risk https://triviumchina.com/our-thoughts/defusing-local-government-debt-risks-whats-in-the-politburos-basket/ Although how to manage the fallout for those small banks remain to be seen.

And as a reader in China who appreciate your work on China, I believe your analysis on China still have ample room to improve if you can take into consideration of the crucial dynamics between central government and local government from an institutional approach. Everything that seems unreasonable to outsiders stems from that. Personally I'd recommend Stanford Prof Xueguang Zhou's book The Logic of Governance in China on this topic.

what is your current take on the investment atractivnes of the Hong Kong/China Markets?