Whatever Happened to Alpha - Part 3

How much beta is in the alpha? (June 18th, 2018)

Part 1: Why haven’t hedge funds made money lately?

Part 2: Easy Money Killed Alpha

It would be great to have actual quality information on the alpha generated by funds, but in order to do that, you need to understand how much beta exposure they have.

Well, when you look at the data, in aggregate, hedge funds look like (moderately) higher Sharpe ratio stocks.

Now, some of this makes sense just from the perspective that alpha is a zero sum game, so any aggregate is going to wash a lot of the alpha out, leaving you with an index that look like the asset weighted portfolio mix of a manager.

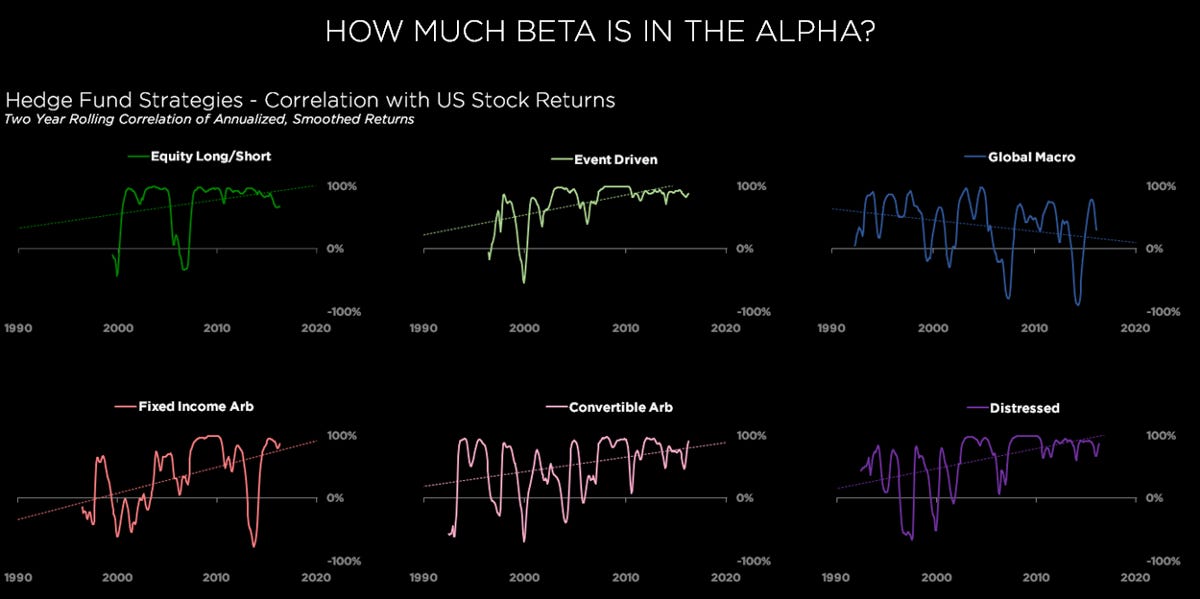

But, again, by looking across hedge fund strategies, it’s possible to see that not only do many strategies seem to be proving a lot of beta with their alpha, but over time more and more of those returns are being dominated by beta.

Which got us thinking. US equities might be a reasonable beta benchmark for a long-short investor, but what about someone playing their trade in global macro?

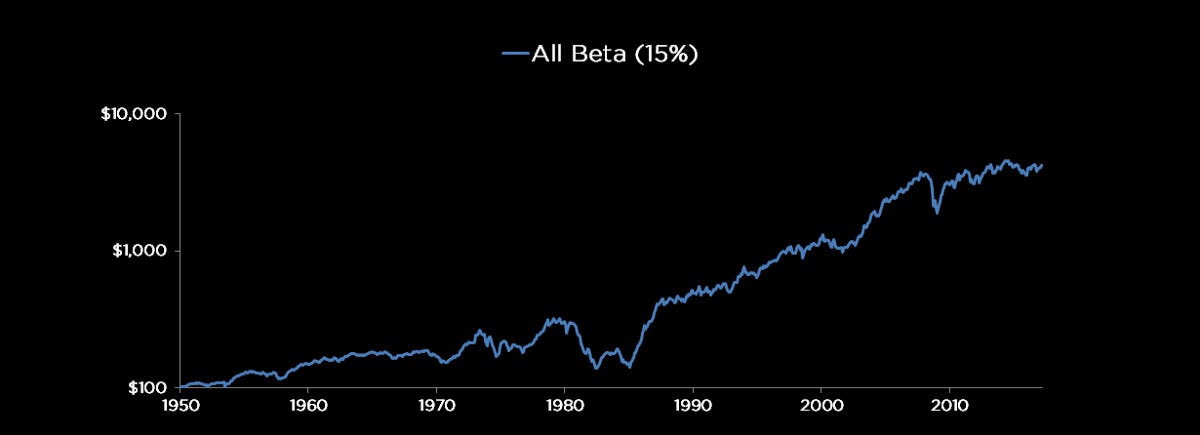

There are as many beta portfolios as there are schools of investing, but for expediency we constructed an “All Beta” portfolio which simply put equal weights on every equity, bonds, commodity and FX market for which we have data.

For US macro funds, a simple beta portfolio is just a diversified mix of all the equity, rates, commodities and currencies they can invest in.

This is what that All Beta portfolio looks like, in excess returns space, when targeted to 15% annual volatility.

Here’s how that portfolio relates to the returns of macro funds, when viewed against a smoothed version of the strategies average Sharpe ratio.

Ok, so we know the answer at least to that question (how much beta in the alpha) is…not zero.

Whether it’s 25% (for an individual firm) or 75% (for the industry aggregate), it’s clear that yes, investors are getting a lot of beta along with their alpha.

In which case, the question becomes, what else is driving that blue line?

Which we will get to, another time…

DISCLAIMER

This article is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, nor does it constitute an offer to provide investment advisory or other services by Snow Ventures. In preparing the information contained in this article, we have not taken into account the investment needs, objectives and financial circumstances of any particular investor. This information has no regard to the specific investment objectives, financial situation and particular needs of any specific recipient of this information and investments discussed may not be suitable for all investors. Any views expressed on this website by us were prepared based upon the information available to us at the time such views were written. Changed or additional information could cause such views to change.