The Regret Trade

Oil and Dollars Up, Everything Else Down

Oil up

Dollar up

Stocks down

Gold down

Copper down

Silver…murdered

This is where it gets real for people.

Whether or not the strait is officially closed, Iran’s strategy of lashing out at everyone and anyone around them is now clear.

Impose maximum pain on the region in order to bring diplomatic pressure to bear on the US (and by association Israel) in order to buy time to refit, rearm and readjust to the new reality.

As discussed in previous rambles ad nauseam, the key problem with this strategy is that it commits to negative sum games in a way that inevitably pushes them further and further away from the ‘reasonable middle.’

When it was a sovereign state trading missiles with another sovereign state, Iran had the benefit of the doubt, as well as ‘international law’ as well as the sneaking suspicion by a) many of the global/European elites, and b) the China/Russia axis, that Israel has disproportionate power relative to their station, and so they could cast themselves as the sole brave regional power willing to stand up to the bully. The irony of a country of 9m bullying a region of 100m+ hostiles notwithstanding.

Then they started killing civilians. Lots of them. Somewhere between 32k and 60k depending on which media you trust (which at this point should be pretty much no one).

By attacking Saudi and the other Gulf states, Iran has ultimately failed in the goals that by my measure kicked off the original October 7th attacks: derail ‘normalization’ of relations between Saudi and Israel via the Abraham Accords. A deal central to the development of an “India-Middle East-Europe” corridor that just so happened to link the two regional rivals and provide a trade link that avoided Iran and the Belt and Road. The irony is that by threatening Gulf security directly, Iran has arguably accelerated the normalization it sought to prevent, giving Saudi a concrete security rationale to deepen partnership with Israel and the West.

As is so often the case in war, this negative sum thinking has inevitably turned the recipients of this animosity against them, and we’re seeing oil production and transportation slow as Saudi and the Gulf States gear up for direct conflict with the regime.

For the Gulf states, this conflict is almost as existential as it is for the mullahs in Iran. Their pitch, for the last two decades, was as bastions of safe, relatively free and luxurious living in the heart of a war torn region. Dubai real estate being the best example.

This pitch isn’t nearly as attractive when folks realize their hideaway is just a drone’s throw away from a suicidal regime.

At this point, the regime’s only friends are a) customers for its oil (China), b) geopolitical allies who don’t seem in a rush to get directly involved (Russia and North Korea), c) various extremist groups, and d) western leftists/liberals who will take any chance to protest Trump’s moves.

Along with the escalation from ‘strikes’ to ‘conflict’ to ‘regional war’ the markets have begun to take notice.

What we saw this morning was the telltale signs of a ‘de-risking event’ where pretty much anything that wasn’t oil or a dollar bank account started to get puked. Classic ‘scramble for liquidity’ perhaps best evidenced less by stocks (which you could also chalk up to the impact from higher energy prices and/or deteriorating growth conditions) but the sell off in precious metals and the surge in the dollar.

Gold (in dollars) falling as folks liquidate their recent winners. Korean favorites like SK Hynix down more than 12% overnight as people look at the chart and go ‘eh, get me out.’ This is what I call the ‘regret’ trade, as people who didn’t appreciate how real the conflict was reprice their book and start thinking about what it means if this lasts more than a news cycle.

Well, as we said yesterday, the real drivers of oil will be whether production facilities are targeted (check) and whether the strait was grinding to a close (check).

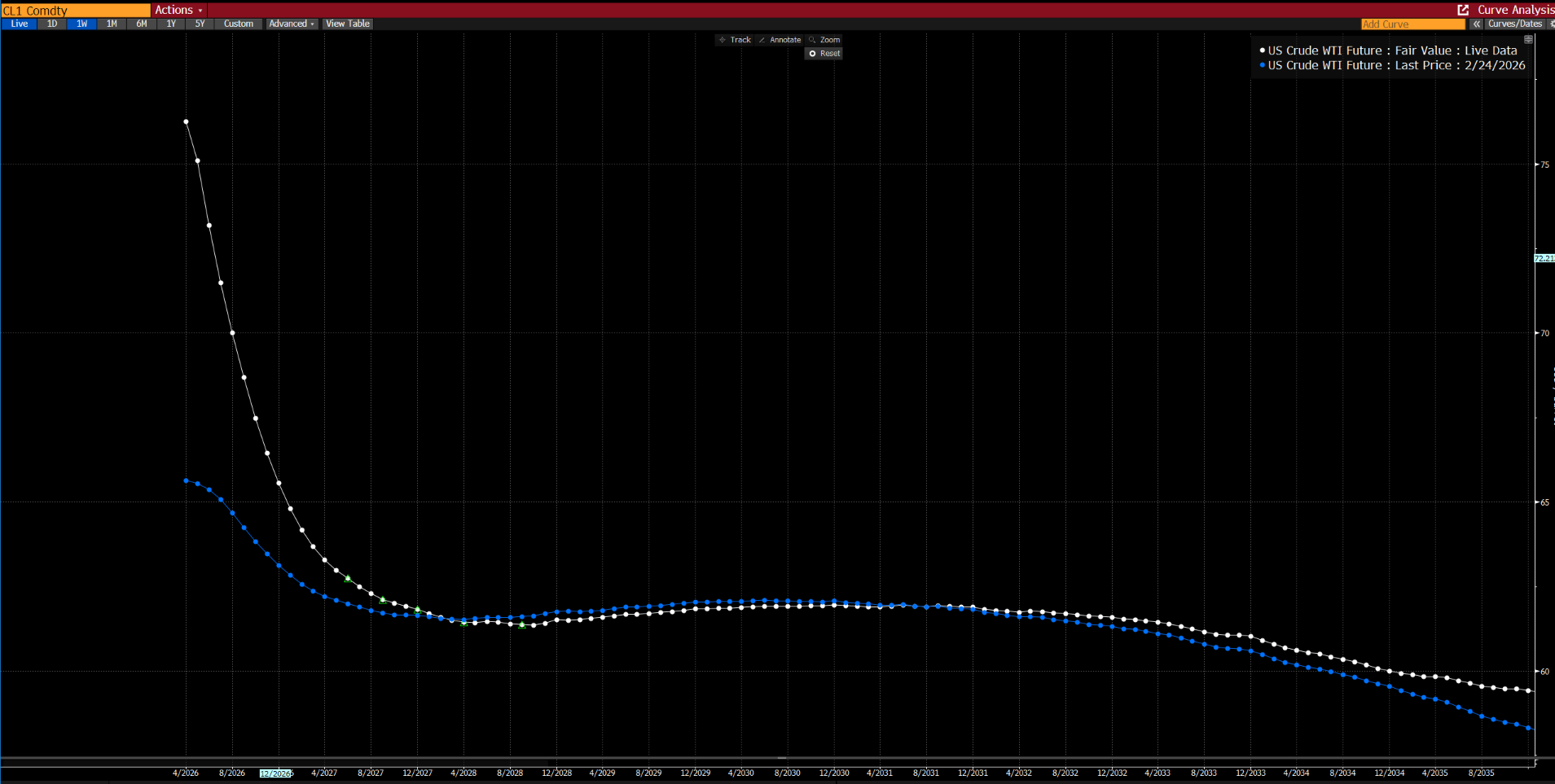

This is where looking at the futures curves helps.

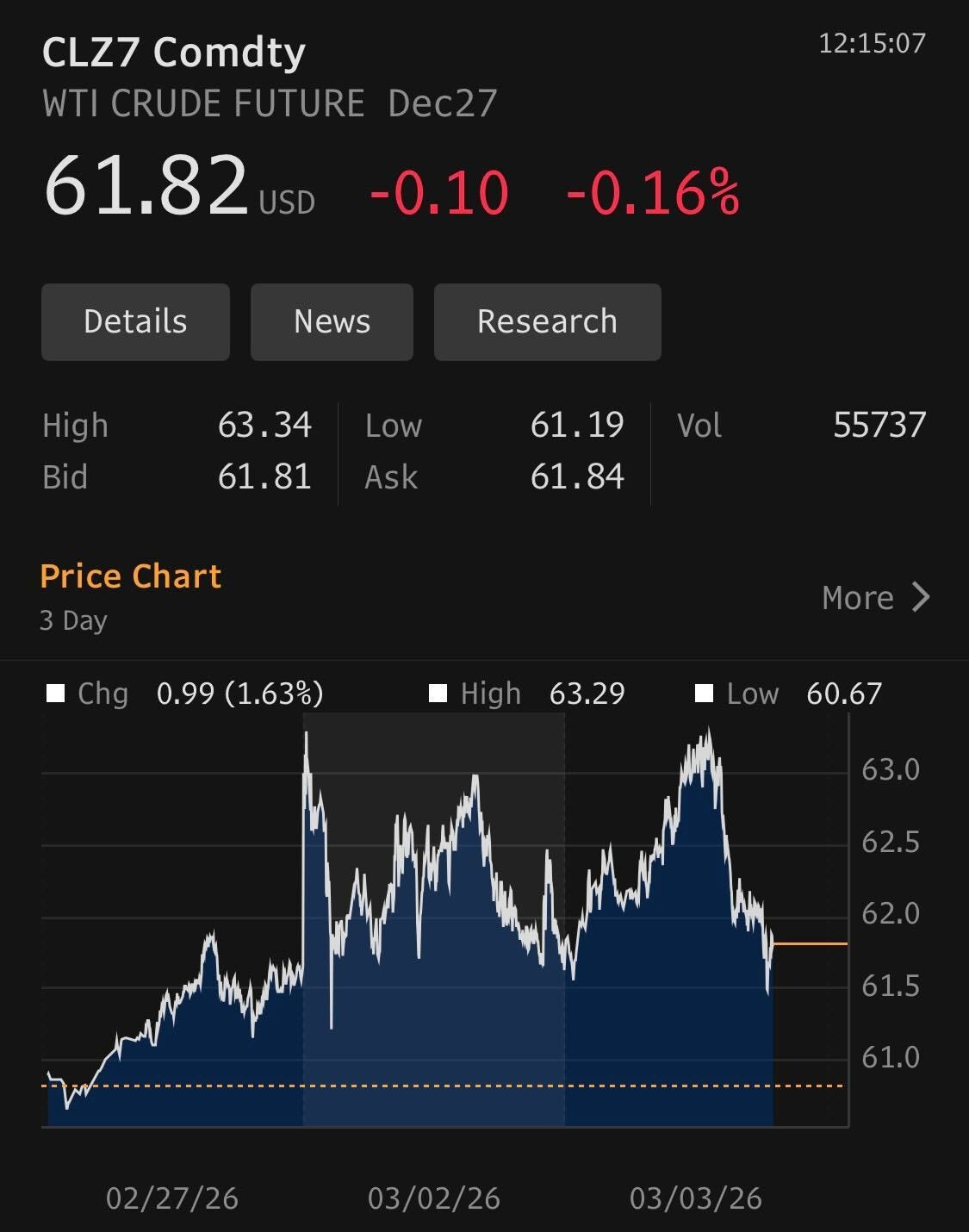

Ironically, this morning US Crude deliverable in December 27 was DOWN on the day.

Showing that folks are still pricing in temporary problems in a ‘well supplied’ market. If you are looking for a trade to protect your book from further deterioration in conditions, this is where I would consider going long oil either in a backwardation trade around where the curve is the most convex or outright in the middle of the curve.

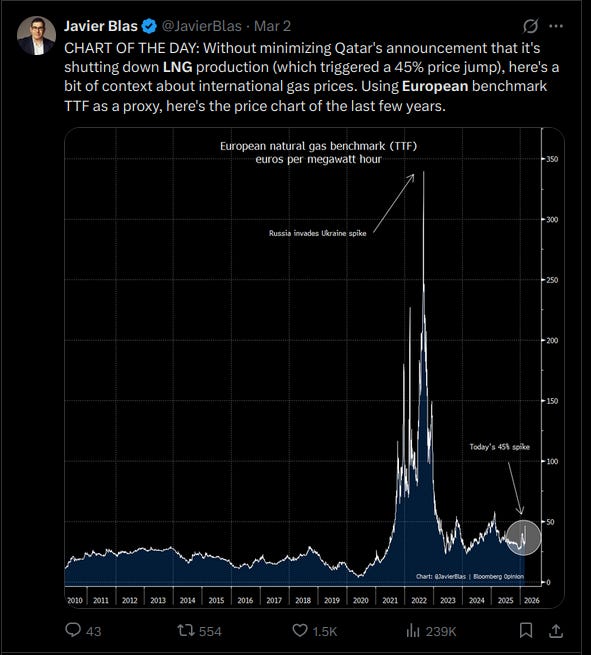

European gas also being the obvious place, as we saw in 2022, it can go much much higher.

Personally, I got caught a bit too long gold (again) from some call options that went in the money while traveling. Yet another reminder that trading options from a mobile phone with three jobs is kind of a dumb idea. As I reflect on where my life is going, these ‘distraction’ mistakes make me appreciate the infrastructure, systems, and trading support that institutions provide. “Do as I say not as I do” vibes for you readers.

Silver, meanwhile, is getting carried out to the woodshed. As both a precious metal and an industrial metal you get selling from both ends. We’re short through our curve trade against some upside options which were just starting to pick up some delta. Now we need to worry about some of our downside put spreads which are picking up some delta down in the 65 range. Good reminder to close your in the money call spreads when they blow through the top strike if you aren’t actively hedging the delta.

We also trimmed our copper leg as a way to position ourselves a bit defensively. Feels like I’m trading short vol on this one a bit but want to save my bullets for where I have more conviction (gold) relative to my views on growth going into a world where energy prices could stay elevated for longer than expectations for high growth can sustain. Also looking at my Korean stocks with a side eye and may trim. This is a good example where your big high confidence trades eat up your risk capacity in a crisis, and likely what is playing out across the board.

“The Dollar is Dead” folks seem awfully quiet today. Good reminder that, again, we live in a world of dollars, and a good example day where ‘double dollar gold’ is a good portfolio protection if you can manage the delta.

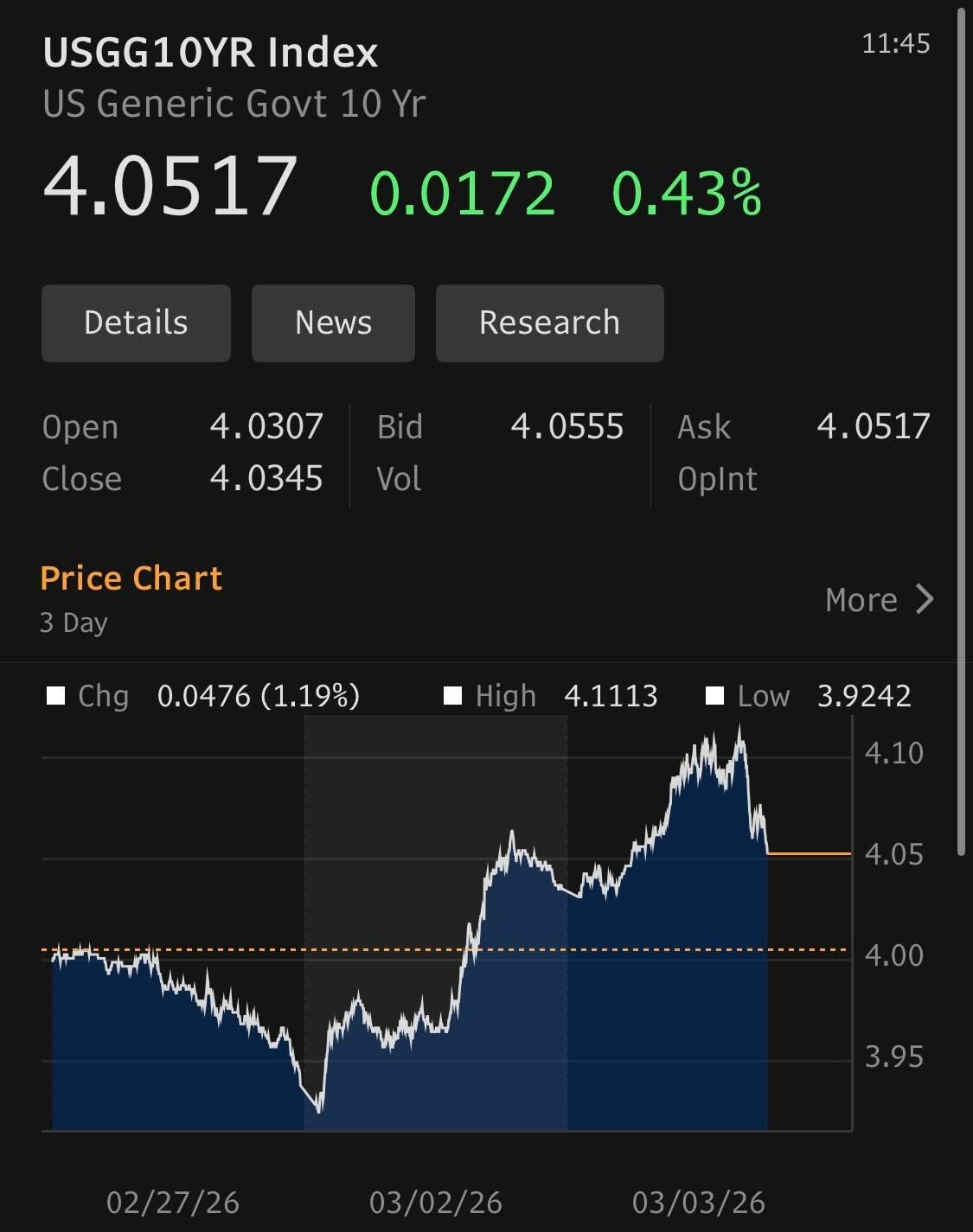

Interestingly bonds were down this morning, as ‘flight to quality’ doesn’t appear to extend to US bonds in an era with rising breakeven inflation via oil and a Fed that doesn’t seem inclined to pull down real yields.

This will change if stocks sell off more, but for the time being worth mentioning. We bought a bit as a test trade this morning just to put our toe in the water. The idea that gold and bonds would fall in a major conflict doesn’t track here. Though recall during 2008 and COVID the scramble for liquidity didn’t leave TIPS unscathed. So if these start getting whacked we’ll likely end up rolling into them in size (though slowly as it’s a widowmaker trade in a crisis).

In terms of your book, you probably woke up with a couple of battle scars this morning. How you react to it, whether you puke your winners, whether you cut the trades that are designed for a regime that just disappeared will determine your month.

This will be a good example of how vol shakes truth out and causes pipes to start leaking. My bet is that even if risk rallied, private credit won’t as folks pick up the things positioned well for the future vs their portfolio excesses of the past.

What those things are, which materials, which components, which software that leads us through the acceleration of geopol and technology that is clearly upon us is still up for grabs. I’m traveling a bunch the next couple of weeks, but will try to put some time into the banks trade in the meantime.

Till next time. Stay safe out there.

Disclaimers

ROFL.

Your geopolitics is garbage mate.

Iran has destroyed the US empire.

The petrodollar is dead.

America has to leave the region now. It has been demilitarised (and denazified)

Enjoyed the read so where would look now areas to invest or are we in a waiting period to see how things flush out