Three years ago, we wrote a piece called “Waiting for the crash, waiting for inflation….”

Two years ago, we showed how in the long run, major inflation is caused by conflict.

Two years and one pandemic later, we got the inflation, we got the dollar tightening, and we got big and growing defaults in the real estate sector.

Tomorrow, Nancy Pelosi is due to fly to Taiwan, and if you listen to Chinese nationalists on Twitter (which I’m afraid to admit I do), you find that they view this as an outrageous provocation. Potentially a unliteral shift away from the “one China policy” enshrined in the vaguely worded “Shanghai Communique,’ published as part of '“Nixon’s goes to China” in ‘72. The same meeting that set the stage for normalization of relations that, for what it’s worth, led to fifty years of benign trade and investment behavior towards Chinese from the West.

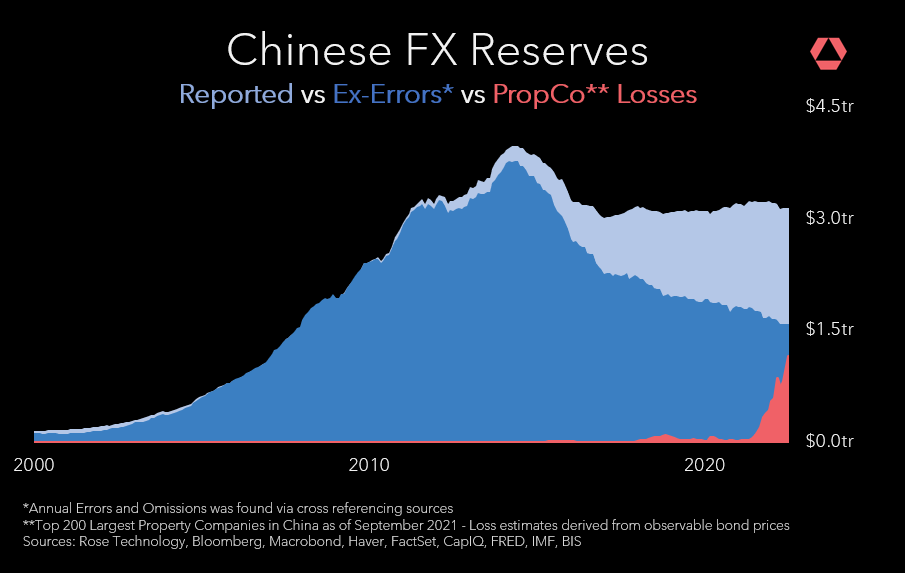

Meanwhile, here at Rose, we continue to watch the canary in the coalmine for the Chinese financial system. Where we see contagion from the default of Evergrande spreading to the broader property sector at home, while nationalists saber rattle abroad.

We now we see almost $2tr of reasons to talk about Taiwan for Chinese policymakers.

How we got here

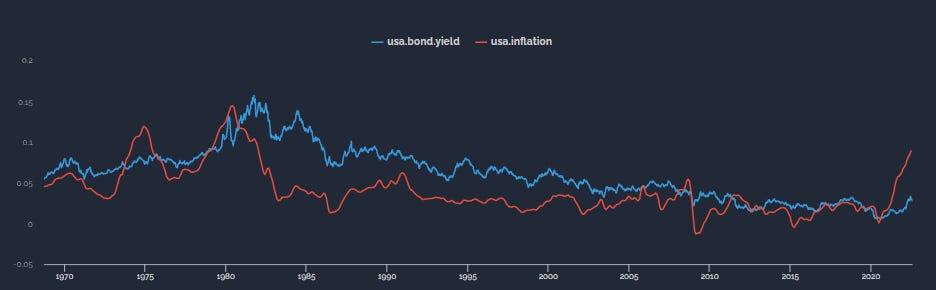

We got here through fifty years of declining global tension, inflation, and interest rates.

Against the backdrop of Volcker tightening in the 80s, was the slow pivot to the west by China and the beginning of the disintegration of the USSR. These two trends lead first to radical increase in globalization in trade, lowering inflation. Second greater globalization in capital markets, which lowered interest rates.

Lower inflation, lower rates, higher growth.

Goldilocks. Unleashed by peace.

As Chinese manufacturing production came online, prices for goods fell for Americans while Chinese purchases of US bonds rose (for use as reserve asset).

The positive feedback loop, lower inflation and further buying support for western risk premiums and asset prices (the “Unicorn Economy”).

Worries of a Chinese banking collapse were shrugged off, as western capital flowed into China to support the status quo - while money was flowing out the backdoor.

Now we have deglobalization everywhere, inflation rising, global tightening, the dollar squeezing, right as the scale of the problem in the Chinese property sector comes into view.

The worst offenders in terms of debt, currently dead or in the process of dying.

Thusfar, the problems have been by and large contained, and pending quarantine of the property problems from the banking system, they just might make it.

But looking closer, are the problems already at an existential point?

Where We Are Today

Against this growing pile of losses are the following small indications of stress in the domestic Chinese banking system.

Small depositors in Henan being arrested, beat up, or put in quarantine for protesting lack of payment by their banks.

Ambiguity remains about ‘who takes the loss’ and how much of China’s FDIC (deposit protection) will really kick in to protect buyers of the $4Tr+ of “Wealth Management Products” which acted as quasi-deposits sold by local banks (thusfar it appears less than $10k, with the usual implementation issues).

A mortgage ‘strike’ from buyers of developments that have seized or taken forever. Considering that the country starts about 5 NYC worth of real estate a year - and those projects can take 10 years on average to complete - that’s a lot of supply hitting the market at distressed prices)

Odd reports from the central bank that financial institutions are “93% safe”

Which begs the question, why are policymakers in China so slow to apportion the losses, if they are so ready with the playbook?

The bull narrative with the Chinese credit crisis was always that the PBoC’s large stock of reserves would enable a swift and rapid restructuring process, ensuring a ‘beautiful deleveraging”.

One where policymakers tighten enough to squash the excesses, but not enough to unleash widespread financial contagion.

So why is it taking so long to unwind Evergrande and the other profligate developers? Why don’t they use their reserves to take the pain and clean up the banks?

Well, we see three potential reasons.

Maybe the prospect for peaceful reunification between the PRC and Taiwan died with the Hong Kong National Security Law. Compounded by the western financial response to Russia’s invasion of Ukraine, which showed that the PBoC might not be able to use those treasuries in the way originally intended.

Maybe the PRC doesn’t have a clean plan to bail out thousands of local banks, which have funneled unsuspecting mom and pop investors into complex deposit-like products that offer neither deposit-like liquidity or deposit-like principal protection.

Finally, maybe those issues become more and more painful to deal with when you account for the fact that of those $3tr of reserves, maybe $1tr+ of assets have already been moved offshore (which we proxy with BoP errors and omissions), and (estimated) property losses already greater than $1tr. Which also happens to be about their level of holdings of US Treasuries.

In short, what if China is almost out of money?

Disclaimers