Another Leg Down?

Investor Update - April 2nd, 2020

Friends,

Not a big update here, we don't have a lot of strong views with respect to market pricing. The system just had a massive shock, and people are still digesting both the pain and the stimulus. We think we likely squeeze higher before going lower, but wouldn't be surprised if that was as far as the cat can bounce.

If you look at the history of financial panics there are clear patterns that emerge. Outside of fluky "technical" jumps like October 1987 or February 2018, volatility in financial markets is usually about time.

Time to figure out and price the pain, time to cleanse the system of rot, and then time for stimulus to flow through and start the healing.

In between we get waves. Waves down as the market wakes up to the fact that the pain is deeper and more fundamental than discounted, and then waves up as the liquidity provided by policymakers flows through to people making intelligent capital decisions.

Oil super contango trade being a classic example here. There comes a point when financial markets are in such panic that you can literally make 20% (by our last count) relatively risk free by pulling oil off the market and just sitting on it. Now you need liquidity to spare to execute (around $55m per tanker by our last count) so this is no mean feat. Which brings in the role of the Fed, to provide the market that liquidity, so that 20% "risk free" arb can be obtained. A productive use of capital and resources on a day when literally the best thing you can do with oil is nothing.

In the meantime, all the other investments out there, they need to compete with that risk free 20%. Those that cannot, well they die on the vine. The organism growing stronger through the generations via evolution.

Which just begs the question, where are we in that cycle now? Have we taken enough pain to flush out the badness, and is there enough stimulation to form a (true) bottom?

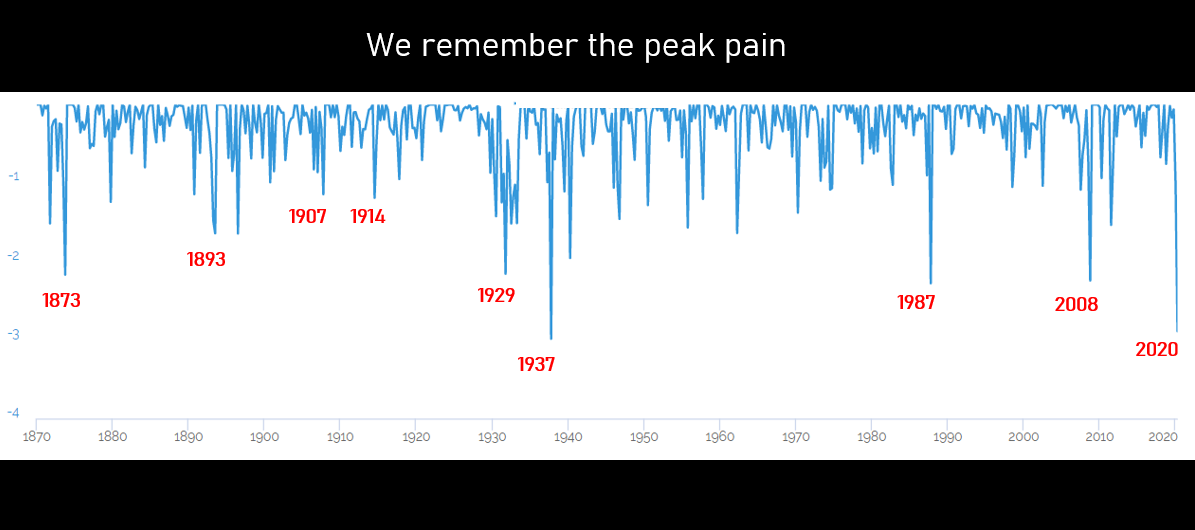

We think the chart below of equity volatility helps frame that question. What's so clear is not just that we are at historic peaks, but that all peaks are not formed differently. 1987 was a really, really bad afternoon, the Great Depression was a bad generation.

To help us get our hands around this concept made a long run indicator of something we call financial chaos.

It includes equity vol (realized and implied), credit spreads (investment grade and high yield) and money market spreads. Simple.

Does a good job highlighting the years of financial chaos we already know by their dates.

Zooming into the more recent history you see an ominous trend/theme as applies to our current conditions.

While the chaos just endured by the market was historic, and while US monetary and fiscal policy stepped in to support markets and restore stability, it's pretty easy to visualize there being another wave down by pattern matching to recent panics.

Asian Financial crisis - two big waves.

DotCom/Enron - a short succession of smaller waves

The 2008 financial crisis and the Eurozone crisis both came in two big waves.

Meaning these follow the pattern we called out above. The first wave identifies the existence of a problem (and wakes policymakers up to provide liquidity/stimulus/restructuring).

The second wave usually shows that the deterioration in financial conditions was systemic. That it's not just a couple bad actors but that the entire system is at risk (or at least feels that way at the time). This forces policymakers to conduct wholesale bailouts of entire portions of the economy, and in the process decide who lives (ie., Morgan Stanley) and who dies (ie., Lehman).

By this point, you know our view, that the biggest long term risk to the global financial system is China.

We believe the western system is healthiest when there are routine, smaller mini-panics which cleanse the system of excessive risk and greed and restore balance between capital and the real economy.

Whereas the Chinese system is structurally, culturally and financially set up to minimize small blow ups at the expense of fewer, but much more dramatic transitions. Whether that's the legacy of imperial trauma from a "Century of Humiliation" or the express political preferences of the children of Mao, we aren't to judge.

What we can say, is that a) there is likely more pain to come in the west, resulting from the macro impacts of the displaced and defaulted, and b) the pain we see in the market today will be remembered as "just the first leg" if policymakers in China were to ever lose control.

So where does that leave us as money managers? Long Gold in China. Long food, moderately short stocks, and waiting out the squeeze.

In short, we are betting on another wave of pain, and we hope we are wrong.